An other mortgage is actually a low-recourse financing, for example the new debtor (or even the borrower’s house) of an opposing financial doesn’t are obligated to pay more than the long term financing equilibrium or perhaps the property value the house, any kind of try shorter. If your debtor or agents regarding their unique estate prefer to sell the house to pay off the reverse mortgage, no assets other than your house is familiar with pay back your debt. Whether your debtor or their unique house wants to keep the property, the balance of your own loan should be paid-in complete.

Opposite mortgage loans are manufactured specifically for elderly home owners, permitting them to benefit from the guarantee he has got gotten within their home.

Having an other mortgage, your borrow secured on the fresh collateral you really have established in your house and don’t need certainly to pay back the loan for as long since you live-in your house as your first quarters, keep the family from inside the good shape, and you can shell out assets taxes and you may insurance rates. You can live in your home and revel in to make zero month-to-month principal and you may attract mortgage repayments.

According to your financial situation, a face-to-face financial provides the possibility to help you stay when you look at the your property but still fulfill your financial financial obligation.

We realize you to opposite mortgages is almost certainly not right for folk, contact us so we might help take you step-by-step through the method and you will address any questions you’ve got.

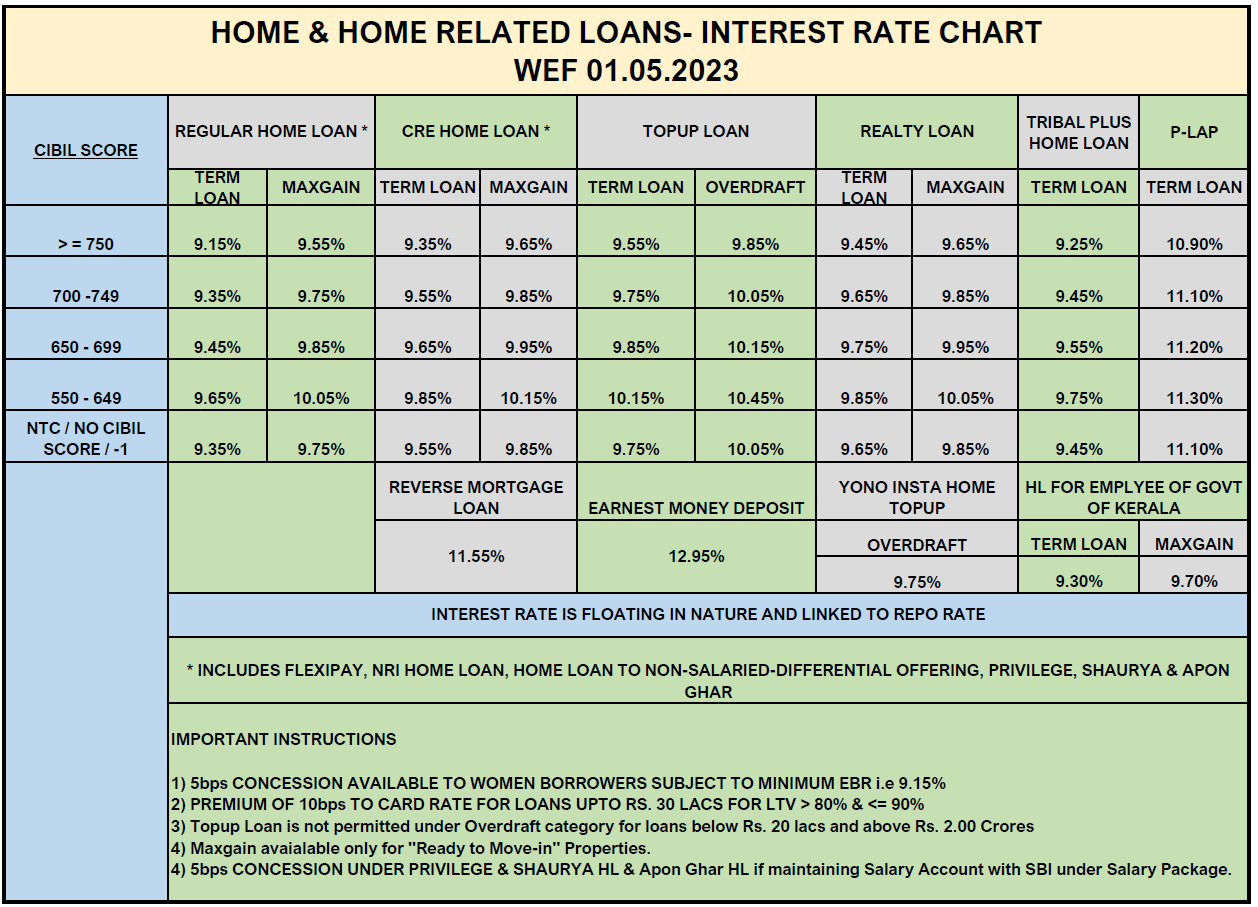

Reverse Mortgage loans against. Traditional Home loan otherwise Family Security Financing

A reverse mortgage is the opposite out of a timeless financial. With a timeless home loan, you borrow money and then make monthly dominating and appeal mortgage payments. Which have an opposing financial, yet not, obtain loan continues based on the worth of your property, age the brand new youngest debtor, in addition to interest of your own loan. You don’t build month-to-month dominating and you can notice mortgage payments having as long as you live-in, maintain your domestic in great condition, and you may shell out possessions taxation and you will insurance coverage. The loan must be paid down when you perish, sell your residence, or no expanded live in the home as your top quarters.

If you are age 62 otherwise more mature, a house Equity Conversion process Home loan (HECM) to buy from Financial from The united kingdomt Mortgage can be an intelligent selection for funding another type of place to phone call house.

Household Security Transformation Financial (HECM) A home Security Transformation Mortgage, or HECM, ‘s the merely contrary home loan covered of the U.S. Authorities, that’s limited as a consequence of an enthusiastic FHA-approved lender.

In place of needing to find conventional financing, borrowers decades 62 and you can elderly should buy another type of quarters when you find yourself getting rid of mortgage repayments* courtesy an other mortgage (Obviously, they will certainly remain accountable for spending property fees and you will necessary homeowners’ insurance). This could assist them to a great deal more conveniently afford an improvement, otherwise save money currency away-of-pouch. Retiring Boomers are choosing to steadfastly keep up a comfortable lives into the a good household that greatest suits their requirements. You own the home, with your name toward label therefore the home get and you will an opposing financial closing is actually rolled toward you to definitely, and then make their procedure easier.

Exactly how much Are Borrowed?

Typically, the greater number of you reside value, brand new old youre, and the decrease the interest rate, the more you’ll be able to in order to borrow. The most which may be borrowed towards the a particular loan system is based on such facts:

- Age the newest youngest debtor during the time of the fresh new mortgage.

- New appraised property value our home.

- Current Rates of interest

Initially Qualification Requirements to possess Opposite Mortgage loans

- Residents need to be 62 years old or older and you can occupy the house or property because their number one house

- The property ily otherwise a two-4 Product property, Townhome, or FHA-approved Condo

- The house must see lowest FHA assets criteria

- Debtor cannot be outstanding toward people federal personal debt

- Completion away from HECM guidance

Every fund are subject to borrowing from the bank approval and additionally credit history, insurability, and you may capacity to render acceptable guarantee. Not all https://cashadvancecompass.com/loans/cash-till-payday-loan/ loans otherwise items are in every says or counties. An opposing financial is actually financing that must be reduced when your house no longer is the primary residence, is available, or if perhaps the home taxation or insurance coverage aren’t reduced. It loan isnt a national benefit. Borrower(s) need to be 62 otherwise earlier. Our home have to be maintained in order to meet FHA Criteria, and you also must still shell out possessions fees, insurance policies and you can property relevant charge or else you will cure your residence.